News

For the last 20 years, investors’ focus for climate solutions has been about providing capital for clean power generation, with significant investment in solar, wind, and storage, as well as mobility. However, decarbonizing the hard-to-abate sectors – the next generation of steel, cement, and clean fuels that are poised to reshape our world – has only just become a mainstream topic for the investment community, despite being one of the largest investment opportunities ahead.

A surge of recent innovation is focused on developing groundbreaking solutions needed to respond to the urgency of the climate crisis, but they need to be scaled rapidly and effectively to realize their full mitigation potential. Unfortunately, the existing funding landscape is not able to provide the capital required for them to innovate and scale across all major emissions sectors – capital that is critically needed.

These next-gen technologies are more than just clean solutions—they’re cutting-edge breakthroughs with the potential to transform entire industries. Imagine concrete made from carbon captured directly from the air, as pioneered by Carbon Upcycling. They have proven that they can deliver cement with 60% less emissions and have demonstrated that they will be below market price for traditionally sourced materials in their full-scale commercial facilities. Or, we could look at the chemical magic of Travertine, which turns mining by-products into valuable molecules, starting with sulfuric acid. Sulfuric acid is the most produced chemical globally outside of refined fuels. They are already working with some of the largest chemical players globally. There’s also Firefly Green Fuels, a company that’s developing sustainable aviation fuel from a very consistent source – human sewage. Innovations like these aren’t just environmentally savvy; they’re defining the cutting edge of industrial technology, poised to create new markets and fuel the future economy with significant efficiencies.

However, most of these technologies all face the same challenge: financing their first pilot or commercial plant. The term most often used to describe these efforts, First-of-a-Kind (FOAK), stems from engineering economics and refers to a new technology, design, or process that has not been fully tested or commercialized. The initial generation of the technology typically costs significantly more than later ones. In practice, FOAK projects typically go through a multi-year derisking process to reach commercialization. This process includes stages such as laboratory-scale validation, pilot testing, demonstration projects, and advanced testing with offtakers, along with other significant engineering and planning efforts that ultimately lead to the construction of a commercial plant. Meanwhile, financing each stage along this journey requires securing significant capital from a very limited set of funding sources.

Solar is a familiar example that illustrates the importance of FOAK investment for the energy transition. In its infancy decades ago, solar energy was considered a FOAK project like the market considers green cement, steel, and fuels today. However, thanks in part to patient and persistent investment through years of R&D and manufacturing learning curves, the levelized cost of energy (LCOE) from solar dropped 85% between 2010 and 2020 ($0.232/kWh to $0.034/kWh). Since 2015, solar energy has regularly had cost parity with natural gas, which in turn has led to a dramatic increase in solar deployment.

The imperative question facing the world now is how do we replicate what we did with solar energy over multiple decades with additional novel climate solutions – such as clean hydrogen, sustainable fuels for aviation and shipping, Long Duration Energy Storage (LDES), green steel, and cement – to deliver the $200 trillion in cumulative investments necessary and meet the urgency of this moment.

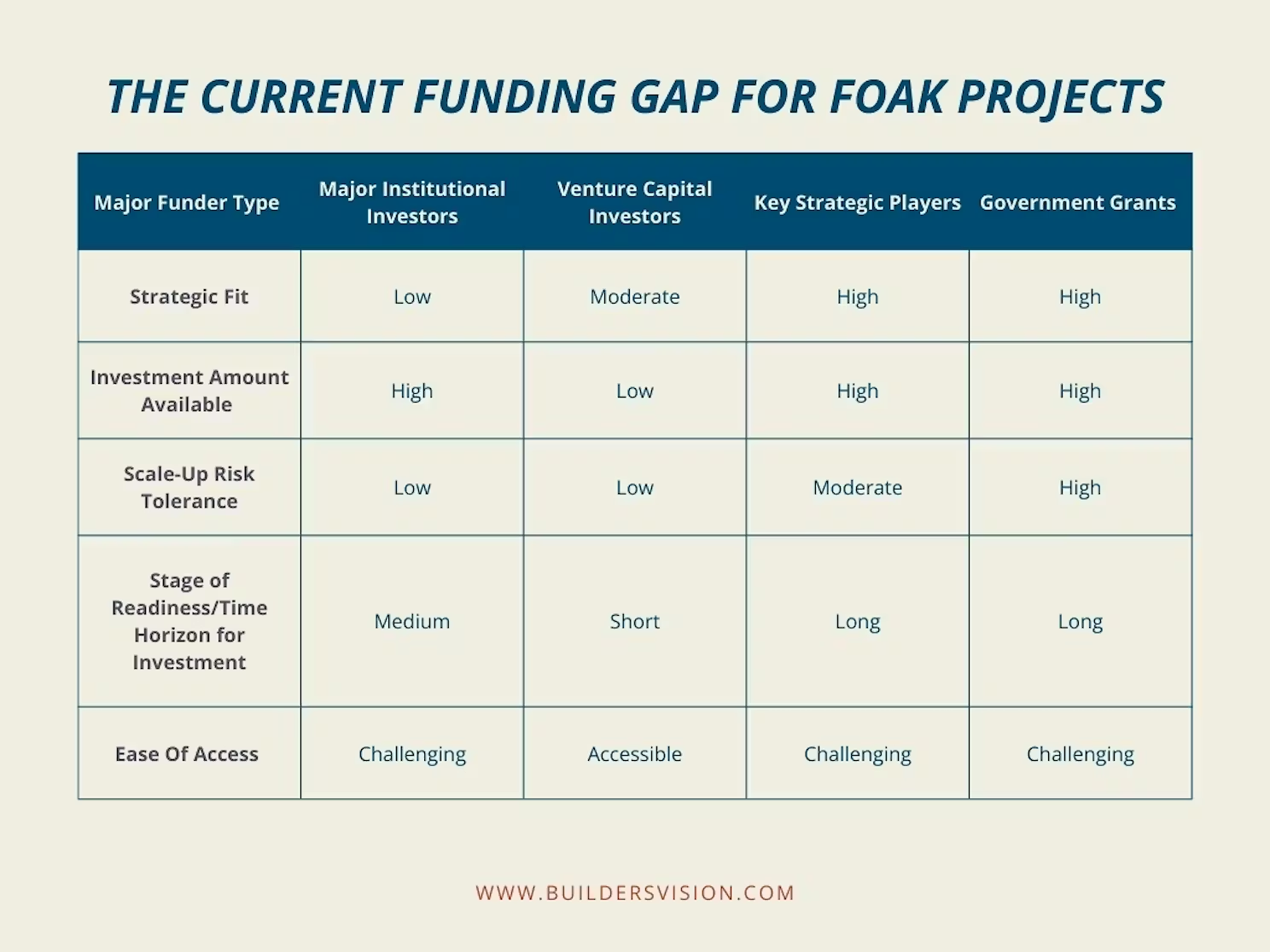

While there is an immense amount of capital focused on the energy transition generally, there’s not enough targeting FOAK project investments specifically. What capital there is isn’t well-suited to the idiosyncrasies of FOAK investing—most investors are simply not oriented to effectively evaluate and fund these kinds of projects. This gap in FOAK funding is symptomatic of what has been called the “missing middle” in energy transition investment. Capital deployed across today’s energy transition market is largely bifurcated across the investing risk spectrum between “infrastructure” capital on one end and venture financing on the other end. While this abundance of venture and infrastructure capital is very welcome, there is also a need for capital focused on supporting FOAK projects that have not yet scaled and de-risked adequately to access infrastructure-type capital.

Scaling an innovation that falls between the two endpoints of the risk spectrum requires founders to build complex capital tables that balance a wide range of objectives. Perhaps the biggest challenge in navigating these funding sources is that most of these funder types will not take a leading role in syndicating and coordinating short-and long-term funding plans.

None of these prospects above in isolation are ideal for a budding innovator. Many FOAK founders are taught by the existing ecosystem that they have to think in terms of the next venture-like fundraising round. They are conditioned to think their primary goal should be acquisition from a big strategic player, which rarely works out as planned nor leads to the optimal deployment to aid the energy transition. Oftentimes, this looks like pivoting to prioritize investment rather than outcomes, founders’ ownership being drastically reduced, or ultimately, failure since the market is not conducive to their model.

The root of the challenge comes down to incentives. Most venture investors, large scale allocators, and big strategic players simply don’t have the structural alignment needed to back FOAK projects in the way that is needed to ensure the innovations that can make the biggest difference in the transition are scaled successfully and their impact maximized. A new approach to investing in these projects is essential for the sector to grow.

At New York Climate Week, Builders Vision co-hosted an event that convened working groups where entrepreneurs and investors – equity investors, debt providers, EPCs (Engineering, Procurement, and Construction), insurance providers, and other key players – discussed these hurdles. Through these discussions, family offices emerged as a key solution to overcoming barriers across sectors.

As the planet continues to warm and the effects of climate change intensify, even the most nascent ideas deserve a chance—they just need backers that are willing to take risks and go the distance to achieve long-term goals.

At Builders Vision, we believe adopting FOAK solutions is essential for staying ahead, driving innovation, ensuring long-term profitability in a carbon-constrained world, and bringing climate solutions down the cost curve. So, we manage an investment portfolio titled Builders Bridge that focuses on catalyzing capital and scaling market solutions into essential, underserved opportunities in oceans, energy, and food and agriculture. We use non-tax advantaged, flexible, patient, and risk-tolerant capital for investments including pre-seed, seed, debt, and project finance. All together we have committed more than $107.5M for FOAK investments, and made 18 investments out of the Builders Bridge Energy Transition portfolio. This includes companies mentioned earlier, such as Travertine, as well as innovative players like EVA, a leader in green cement, and UbiQD, a quantum dot manufacturer whose work was recognized with the 2023 Nobel Prize in Chemistry.

In addition to investing, we are also working to build a community of co-investors that can help accelerate the design, development, and deployment of FOAK plants. We are also building a database of FOAK projects and investors that can help uncover best practices and foster the exchange of powerful ideas that will enable investors to break into the hardest-to-abate industries — like steel, cement, chemicals, and more.

Investing in the de-risking phase often requires an approach that differs from the equity focused, venture community that exists in climate hard-tech. To address this, we have created a new type of hybrid investment that combines the structure of later stage project financing, with some of the upside that should exist given the early stage risk. We have developed a flexible debt security that provides downside protection, maintains upside, and can be easily adjusted to accommodate other investor needs. Most importantly, this note is designed to be easily modified to match other investor’s return expectations. Catalyzing others is essential for scale.

Our key illustrative terms include:

Other family offices can adopt similar strategies to help these businesses truly scale. Like Builders Vision, they can be flexible in how they structure investments to meet the unique needs of each project and are agile enough to engage with the day-to-day strategic operations of the companies. They can also partner with other family offices to pool resources and knowledge.

We are proud to lead the charge in creating a supportive ecosystem for FOAK development, and many more family offices can—and should—consider joining us. The future of the energy transition depends on it.